Global Vacuum Insulation Panels Market Forecast 2026–2036: Market Expansion Driven by Energy Efficiency Standards

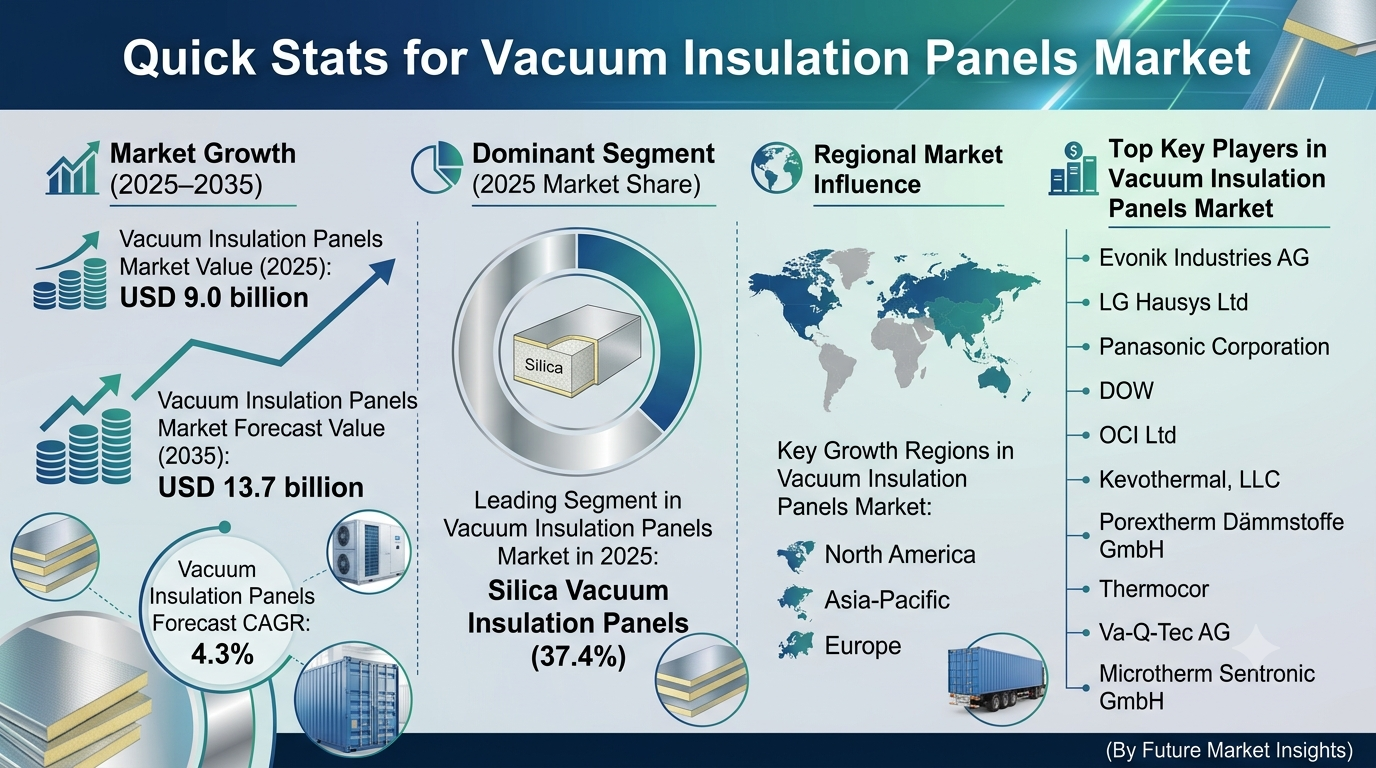

The global vacuum insulation panels market is projected to witness strong expansion over the next decade, supported by tightening energy efficiency regulations and rising infrastructure development across major economies. The market is expected to grow steadily, reaching approximately USD 13.7 billion by 2036, registering a CAGR of 4.3%, according to the latest analysis by Future Market Insights (FMI). Market growth is being shaped by increasing government mandates for carbon reduction, growing consumer awareness regarding sustainable building materials, and rapid adoption of advanced thermal insulation technologies. Vacuum insulation panels (VIPs) have evolved from niche alternative solutions into essential components across the construction, refrigeration, and logistics sectors. While traditional insulation materials continue to occupy high volumes, industries are increasingly integrating advanced VIP systems to comply with modern environmental expectations and achieve superior thermal performance.

Global Vacuum Insulation Panels Market Snapshot (2026–2036)

Market size outlook toward 2036: USD 13.7 billion

Forecast CAGR: 4.3%

Dominant material category: Silica vacuum insulation panels (37.4% share)

Fastest-growing country segment: China (~5.8% CAGR)

Key growth regions: North America, Asia-Pacific, Europe

Primary demand channel: Building construction and refrigeration systems

Momentum in the Market

Beginning from steady industrial adoption levels, the global vacuum insulation panels market demonstrates accelerated growth throughout the forecast period as sustainability compliance becomes mandatory across multiple countries. Between 2026 and 2036, expanding commercial construction and rising investments in temperature-controlled transport are expected to significantly boost demand for ultra-thin, high-performance insulation systems. Increasing urbanization and higher space optimization constraints in modern architecture are encouraging developers and manufacturers to prioritize VIP technologies. From 2036 onward, innovation in alternative core materials and integration with advanced structural panels is expected to further strengthen market expansion. Smart manufacturing processes capable of extending the lifespan and improving the mechanical durability of vacuum panels are emerging as key differentiators for leading industry models.

The Reasons Behind the Market’s Growth

Demand for vacuum insulation panels is rising due to multiple structural and technological factors reshaping the global industrial and construction ecosystems.

Stringent Government Energy Regulations

Governments worldwide are enforcing mandatory building energy codes to reduce green emissions and align with net-zero sustainability targets. VIPs are increasingly becoming a non-negotiable component in premium retrofitting and ultra-low energy building designs.

Growing Cold Chain Infrastructure

Rapid expansion of global logistics hubs, particularly for pharmaceutical storage and fresh food distribution, is driving large-scale commercial adoption of premium insulated containers.

Rising Demand for Space-Saving Systems

Architects and manufacturers are prioritizing insulation materials that deliver maximum thermal performance with minimal thickness, allowing for enhanced interior volume and appliance capacity.

Expansion of Home Appliances Market

The rise of energy-star certified domestic refrigerators and freezers is creating demand for custom-shaped vacuum insulation profiles tailored to modern appliance layouts.

Top Segment Application Type

Silica-Based Core Leads Market Demand

Silica vacuum insulation panels account for the majority of installations across global markets, supported by the material's superior thermal resistance, consistent reliability, and established manufacturing maturity.

Design and Regional Analysis

Flat panels: ~58.6% market revenue share driven by universal deployment in construction walls and doors.

Special shaped panels: Accelerating adoption supported by complex industrial equipment geometries.

China market: ~5.8% CAGR, the highest growth country driven by localized manufacturing hubs.

India market: ~5.4% CAGR, fueled by rapid urbanization and cold-chain scaling.

Regional Development: Manufacturing Ecosystems Drive Expansion

The global production framework for vacuum components is rapidly evolving, supported by cost-efficient operations and expanding commercial infrastructure.

Germany: Western Europe production leader focused on high-performance passive house standards.

United States: Expanding commercial retrofits, advanced medical storage, and temperature-controlled packaging networks.

Japan & South Korea: Established high-tech manufacturing centers supporting next-generation appliance integration.

Localized joint ventures between material suppliers and engineering firms are improving raw core availability while reducing structural costs and accelerating regional technology distribution.

Challenges, Trends, Opportunities, and Drivers

Drivers

Mandatory building codes and carbon targets

Rising cold chain logistics requirements

Increasing emphasis on space optimization

Expansion of domestic appliance manufacturing

Opportunities

Integration with advanced aerogel composites

Custom-engineered automotive battery thermal management

Sustainable and recyclable encapsulation films

Adoption in modular and pre-fabricated structures

Trends

Transition toward long-life getter materials

Automation in vacuum sealing verification

Increased deployment in high-density urban building retrofits

Eco-friendly core material development

Challenges

Higher initial procurement costs compared to traditional fiberglass

Fragility and handling risks during transit and installation

Compliance with evolving regional safety and fire standards

Country Growth Outlook (Global Region)

The market’s growth trajectory is closely tied to domestic infrastructure investments and energy regulation enforcement across key economies:

China: Manufacturing leadership and massive urban development projects.

India: Rapidly expanding food and pharmaceutical logistics networks.

Germany: Frontrunner in building insulation mandates and sustainable architecture.

United States: Rising adoption in corporate commercial real estate retrofits.

The Competitive Environment

The global vacuum insulation panels market is moderately consolidated, with specialized material innovators and global chemical providers competing through proprietary designs, automated scale, and regulatory compliance. Leading companies include:

Evonik Industries AG

LG Hausys Ltd

Panasonic Corporation

DOW

OCI Ltd

Kevothermal, LLC

Porextherm Dämmstoffe GmbH

Va-Q-Tec AG

These players are investing heavily in automated core production, lightweight barrier foils, and extended-life designs while forming partnerships with construction and appliance OEMs to secure steady supply agreements and scale output.

Future Outlook: Toward Sustainable and Efficient Insulation

The vacuum insulation panels market is entering a transformative decade shaped by automation, space limitations, and strict green compliance. Future panel designs are expected to function as integrated thermal envelopes working alongside smart climate management architectures. As industrial and construction markets mature and energy limitations strengthen, vacuum insulation panels will remain central to achieving highly sustainable and resource-efficient infrastructure networks throughout the world.

For a comprehensive strategic outlook and detailed analysis of technological developments shaping the industry, readers can explore the full report on the official Future Market Insights website:

https://www.futuremarketinsights.com/reports/vacuum-insulation-panels-market