Solder Materials Market Forecast 2025–2035: Market Expansion Driven by Electronics Growth

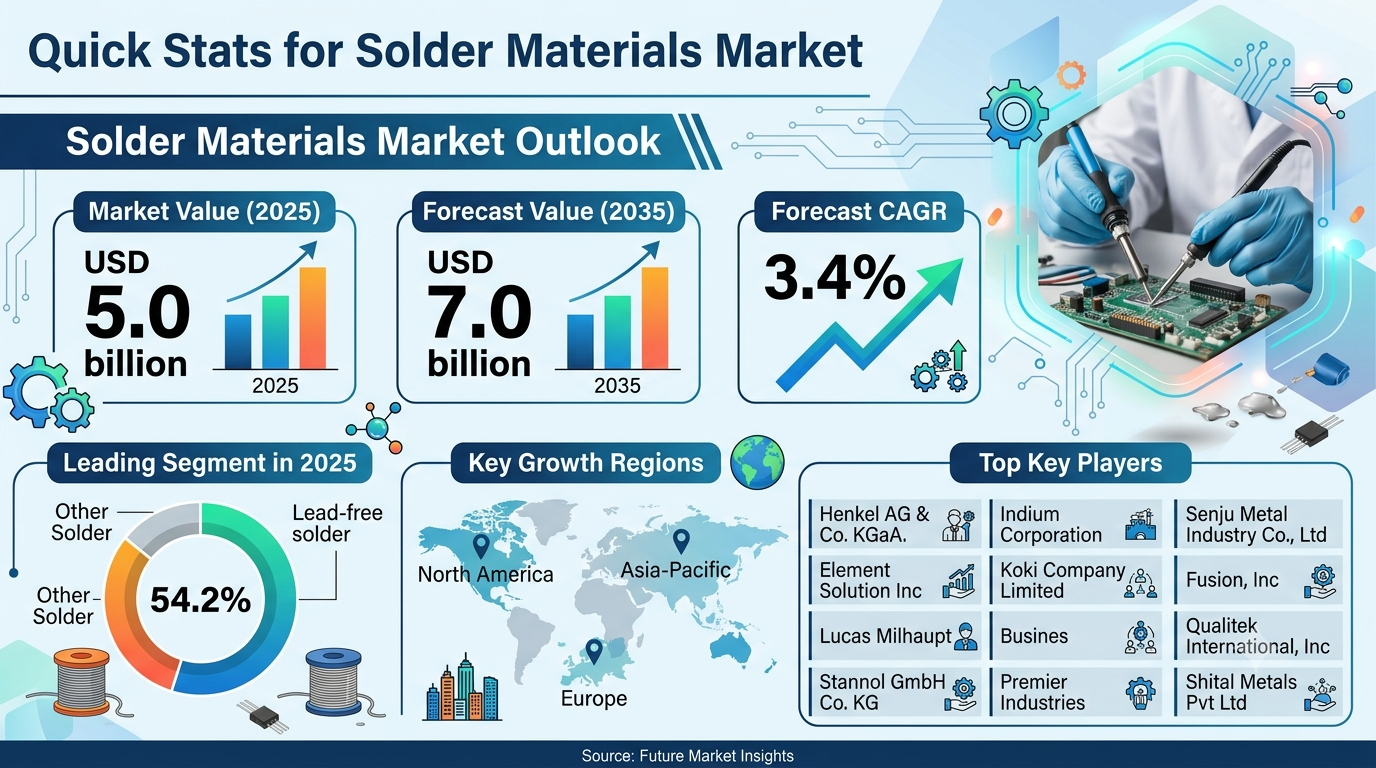

The global solder materials market is projected to witness steady expansion over the next decade, supported by accelerating demand for miniaturized electronics and tightening environmental safety regulations. The market is expected to grow steadily, reaching approximately USD 7.0 billion by 2035, up from USD 5.0 billion in 2025, registering a CAGR of 3.4%, according to the latest analysis by Future Market Insights (FMI).

Market growth is being shaped by increasing regulatory mandates for hazardous substance reduction, growing production of electronic devices, and rapid adoption of advanced automotive technologies like electric vehicles (EVs). Solder materials have evolved from basic assembly components into highly precise formulations essential for ensuring the thermal and mechanical reliability of modern high-density electronics. While traditional lead-based solders are still utilized, manufacturers are increasingly transitioning to advanced, eco-friendly alternatives to comply with global environmental standards and improve crash, vibration, and thermal protection outcomes in harsh operating environments.

Solder Materials Market Snapshot (2025–2035)

Market size outlook toward 2035: USD 7.0 billion Forecast CAGR: 3.4% Dominant product category: Lead-free solder (54.2% market share) Fastest-growing form segment: Solder Paste (~29.8% market share) Key growth regions: North America, Asia-Pacific, Europe Primary demand channel: Electronics Manufacturing and PCB Assembly

Momentum in the Market

Beginning from steady regional adoption levels, the global solder materials market demonstrates accelerated growth throughout the forecast period as regulatory compliance becomes mandatory across multiple countries. Between 2026 and 2035, expanding smartphone production, smart home appliances, and automotive electronic architectures are expected to significantly boost demand for integrated joining materials. Increasing urbanization and higher dependency on digital infrastructure are encouraging governments and technology giants to prioritize stable component protection technologies.

From 2035 onward, innovation in intelligent semiconductor packaging and integration with advanced driver-assistance systems (ADAS) is expected to further strengthen market expansion. Refined solder materials capable of adapting to higher thermal cycles and preventing mechanical joints from cracking are emerging as key differentiators in high-end electronic models.

The Reasons Behind the Market’s Growth

Demand for solder materials is rising due to multiple structural and technological factors reshaping the global hardware ecosystem.

Stringent Environmental and Safety Regulations Governments across major manufacturing nations are enforcing mandatory lead-free installation requirements through directives like RoHS and WEEE to reduce electronic waste toxicity. Solder formulations are increasingly becoming a non-negotiable component in compliance auditing.

Growing Electronics Production and Sales Rapid expansion of consumer tech hardware and automotive manufacturing hubs, particularly in the Asia-Pacific region, is driving large-scale OEM adoption of advanced solder systems.

Device Miniaturization Trends As components get smaller and denser, manufacturers are prioritizing advanced solder pastes and specialty alloys that ensure zero defects and high precision during joint formation.

Electric Vehicle Expansion The rise of electric vehicles is creating a massive requirement for high-conductivity solder alloys capable of handling the heavy electric powertrain components and battery management systems.

Top Segment Application Type

Lead-Free Solder Leads Market Demand Lead-free materials account for the majority of installations across industrial and consumer electronics markets, supported by private quality assurance programs and strict regulatory mandates requiring the elimination of toxic heavy metals in new consumer goods.

Form and Process Analysis Solder Paste: ~29.8% market share driven by surface-mount technology (SMT) expansion. Wave and Reflow Processes: ~47.3% market share supported by high-speed assembly automation. Specialty Wires & Preforms: Growing demand with rising premium aerospace penetration. Low-Residue Flux Solders: Expanding fastest due to the elimination of post-cleaning steps in manufacturing.

Regional Development: Asia-Pacific Manufacturing Ecosystem Drives Expansion

The global supply chain relies heavily on localized manufacturing partnerships between chemical suppliers and regional hardware builders to optimize electronic cost efficiencies.

Asia-Pacific: The undisputed global leader in high-volume semiconductor assembly and electronic component exports. North America & Europe: Expanding high-reliability production capacities in medical electronics, aerospace engineering, and defense infrastructure. Emerging Hubs: Local assembly centers in Latin America and Eastern Europe are slowly expanding their localized capabilities to meet localized regional demand.

Challenges, Trends, Opportunities, and Drivers

Drivers Mandatory lead-free electronic regulations Rising production of smartphones, EVs, and consumer appliances Increasing requirement for high thermal conductivity joints Expansion of automated surface-mount technology lines

Opportunities Specialty alloys for harsh environment aerospace systems Low-temperature soldering to protect fragile components Recyclable and sustainability-focused solder formulations Integration with high-density semiconductor packages

Trends Transition toward micro-fine pitch solder paste applications Nitrogen-assisted reflow soldering processes Increased adoption of multi-alloy paste configurations Eco-friendly, water-soluble flux chemistry innovations

Challenges Raw material price volatility of tin, silver, and copper Complex wetting requirements for lead-free compositions Compliance with overlapping international environmental rules

The Competitive Environment

The solder materials market is moderately consolidated, with global chemical and material technology providers competing through continuous innovation, localized distribution chains, and stringent regulatory compliance. Leading companies include:

Henkel AG & Co. KGaA Indium Corporation Senju Metal Industry Co., Ltd. Element Solutions Inc. Koki Company Limited

These players are investing heavily in low-melting-point formulations, ultra-fine powders, and EV-compatible thermal joining materials while forming deep development partnerships with tier-one electronics manufacturing service (EMS) providers to accelerate product deployments.

Future Outlook: Toward Intelligent and Safer Mobility

The solder materials market is entering a transformative decade shaped by automation, green manufacturing, and high-frequency connectivity such as 5G and satellite networks. Future solder materials are expected to function as highly specialized thermal interfaces working alongside automated optical inspection platforms. As electronic assembly tech matures and environmental awareness strengthens, advanced solder solutions will remain central to achieving safer, greener, and more reliable digital ecosystems globally.

For a comprehensive strategic outlook and detailed analysis of technological developments shaping the industry, readers can explore the full report on the official Future Market Insights website: https://www.futuremarketinsights.com/reports/solder-materials-market