EV Traction Inverter Market on Track to USD 30.7 Billion by 2035

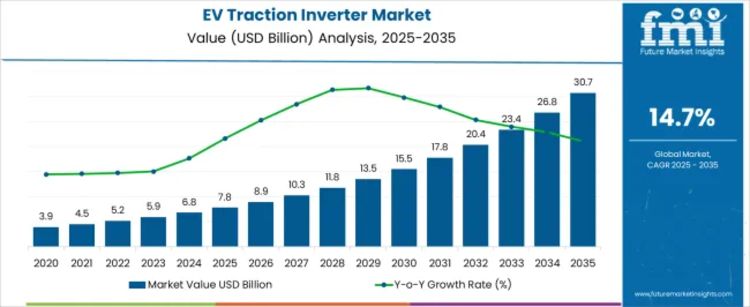

the global EV traction inverter market is entering a period of accelerated growth, driven by the rapid adoption of electric vehicles, advancements in semiconductor technologies, and increasing investments in automotive electrification. According to the latest analysis by Future Market Insights, the market is projected to grow from USD 7.8 billion in 2025 to USD 30.7 billion by 2035, registering a robust CAGR of 14.7% during the forecast period.

As governments worldwide intensify efforts to reduce carbon emissions and consumers increasingly embrace electric mobility, traction inverters have become indispensable components within modern EV powertrains. These systems convert direct current (DC) from batteries into alternating current (AC) required to power electric motors, making them central to vehicle efficiency, performance, and driving range.

Get detailed market forecasts, competitive benchmarking, and pricing trends: https://www.futuremarketinsights.com/reports/sample/rep-gb-24724

Featured Snippet: Key Market Insights

- Market Size (2025): USD 7.8 Billion

- Forecast Value (2035): USD 30.7 Billion

- CAGR (2025–2035):7%

- Leading Segment: Battery Electric Vehicles (BEVs) – 52.4% Market Share

- Top Growth Regions: Asia-Pacific, North America, Europe

- Key Technologies: Silicon Carbide (SiC), Gallium Nitride (GaN), IGBT-Based Inverters

- Core Applications: Electric Vehicle Propulsion and Power Management Systems

Market Overview: Power Electronics Become the Backbone of Electric Mobility

The EV traction inverter market is witnessing significant momentum as automotive manufacturers prioritize energy efficiency, performance optimization, and longer driving ranges. With electric vehicle production expanding across passenger and commercial vehicle segments, demand for advanced traction inverter technologies continues to rise.

Traction inverters play a vital role in managing power flow between batteries and electric motors. Modern inverter systems improve acceleration, regenerative braking performance, energy utilization, and overall vehicle reliability. As EV manufacturers transition toward higher-voltage architectures and more sophisticated powertrain designs, inverter technologies are evolving into highly engineered systems that significantly influence vehicle competitiveness.

The market is expected to experience particularly strong expansion between 2030 and 2035, supported by large-scale EV manufacturing, wider adoption of premium electric vehicles, and increased deployment of advanced semiconductor materials.

Key Market Drivers

- Rising Global Electric Vehicle Adoption

Growing environmental awareness, favorable government policies, and expanding charging infrastructure are accelerating EV adoption worldwide. This trend is directly boosting demand for high-performance traction inverters capable of delivering greater efficiency and power density.

- Advancements in Semiconductor Technologies

The transition from traditional silicon-based devices toward wide-bandgap semiconductors is transforming inverter performance.

Key innovations include:

- Silicon Carbide (SiC) power modules

- Gallium Nitride (GaN) switching technologies

- High-frequency power conversion systems

- Advanced thermal management solutions

These technologies reduce energy losses, improve switching efficiency, and support compact inverter designs.

- Automotive Electrification Initiatives

Automakers are investing heavily in electrification strategies to meet emission regulations and sustainability goals. As electric powertrains become mainstream, traction inverters are emerging as one of the most critical components in achieving vehicle efficiency and performance targets.

Regional Insights

North America

North America remains a key market for EV traction inverters due to increasing sales of electric SUVs, pickup trucks, and commercial fleets.

Growth is supported by:

- Strong EV adoption rates

- Government incentives for clean transportation

- Investments in battery manufacturing facilities

- Growing deployment of SiC-based inverter technologies

The United States continues to drive regional demand through innovation in electric mobility and advanced automotive engineering.

Europe

Europe's market growth is anchored by aggressive decarbonization goals and stringent vehicle emission regulations.

Key growth factors include:

- Expansion of electric vehicle manufacturing

- Investment in semiconductor innovation

- Strong automotive R&D ecosystem

- Government-backed electrification initiatives

Countries such as Germany, France, and the United Kingdom remain important centers for next-generation power electronics development.

Asia-Pacific (Fastest Growing Region)

Asia-Pacific is expected to dominate market growth throughout the forecast period.

The region benefits from:

- Rapid industrialization and urbanization

- Strong EV manufacturing ecosystems

- Government incentives supporting electrification

- Expansion of battery and semiconductor production

China is projected to register a CAGR of 19.8%, while India is expected to grow at 18.4%, making them among the fastest-growing markets globally.

Technology Trends Shaping the Future

Several technological innovations are redefining traction inverter capabilities:

Silicon Carbide (SiC) Inverters

SiC technology enables:

- Higher switching frequencies

- Improved thermal performance

- Reduced power losses

- Extended driving range

Integrated Power Electronics

Manufacturers are increasingly combining:

- Traction inverters

- Onboard chargers

- DC-DC converters

into compact, integrated modules that reduce weight and system complexity.

AI-Enabled Power Management

Artificial intelligence is enhancing inverter performance through:

- Real-time power optimization

- Predictive diagnostics

- Energy efficiency improvements

- Advanced thermal control strategies

High-Voltage Architectures

The shift toward 800V and higher-voltage EV platforms is driving demand for advanced inverter systems capable of handling greater power levels while maintaining efficiency.

Challenges in the Market

High Cost of Advanced Semiconductor Materials

Although SiC and GaN technologies offer substantial performance benefits, their manufacturing costs remain relatively high compared to conventional silicon solutions.

Supply Chain Constraints

Global semiconductor shortages and component supply disruptions continue to create challenges for manufacturers seeking to scale production.

Reliability and Safety Requirements

Automotive-grade traction inverters must meet stringent reliability, durability, and safety standards, increasing development complexity and production costs.

Opportunities: Next-Generation Electric Mobility

The market presents significant opportunities for innovation and expansion through:

- Silicon Carbide-based inverter adoption

- High-performance EV platforms

- Commercial vehicle electrification

- Integrated drivetrain architectures

- AI-driven energy management systems

- Advanced cooling and thermal technologies

Companies investing in these areas are expected to gain a competitive advantage as EV adoption accelerates globally.

Segmentation Insights

By Propulsion Type

Battery Electric Vehicles (BEVs)

- Largest market segment with 52.4% share in 2025

- Strong demand for efficient power conversion systems

- Increasing global adoption of fully electric vehicles

- Focus on range optimization and performance enhancement

By Output Power

≥130 kW Segment

- Expected to account for 58.1% of market revenue in 2025

- Driven by electric SUVs, trucks, and commercial vehicles

- Supports high-performance drivetrain applications

By Technology

IGBT-Based Inverters

- Forecast to capture 63.7% market share in 2025

- Strong balance of efficiency and cost-effectiveness

- Widely adopted across mainstream EV platforms

Competitive Landscape

The EV traction inverter market is highly competitive, with companies focusing on semiconductor innovation, power density improvements, and integrated powertrain solutions.

Leading Companies

- Mitsubishi Electric Corporation

- Continental AG

- DENSO Corporation

- Hitachi Astemo Ltd

- Robert Bosch GmbH

- Toyota Industries Corporation

- Valeo SE

- Vitesco Technologies

- ZF Friedrichshafen AG

These organizations continue to invest in next-generation inverter technologies, silicon carbide platforms, advanced cooling systems, and integrated electric drive solutions.